Types of Stablecoins Explained: How USDC, USDT, and Others Work

Stablecoins are digital assets built to do something most cryptocurrencies can’t: stay stable.

Pegged to a fiat currency, usually the U.S. dollar, they’re designed to hold value even when the rest of the market swings wildly.

They aim to consistently hold a fixed value, usually 1 US dollar, regardless of market turbulence.

That price stability makes them useful for everything from fast trading and cheap cross-border payments to staying in cash without actually leaving crypto.

Traders use them to hedge or move capital efficiently. DeFi protocols use them as base liquidity.

And increasingly, institutions use them to settle millions in volume without touching a bank.

They’ve quietly become one of the most important building blocks in digital finance. But behind the $1 peg, there’s a lot going on: and not every stablecoin is built the same way.

Some are backed by actual dollars. Others rely on smart contracts. A few run entirely on algorithms, and sometimes fall apart.

As regulation heats up and the financial world inches closer to tokenized dollars, understanding how stablecoins work isn’t optional. It’s foundational.

Let’s break down how they hold value, why investors care, and where they might fit into the next phase of global finance.

Why This Matters for You:

✅ You get a volatility-free tool in a market built on chaos. Stablecoins give you staying power (earning, lending, hedging) without having to YOLO your savings into whatever altcoin Twitter’s shilling today.

✅ You can trade like a sniper, not a bagholder. Stablecoins let you exit risk assets in seconds without leaving the crypto ecosystem, giving you firepower for the next play without touching your bank account.

✅ You unlock next-gen finance at your own pace. From staking in DeFi to sending cash across borders in less than a minute, stablecoins are the utility layer powering the real, usable side of crypto.

🤔 Trust isn’t programmable. Whether it’s Circle’s audits or Tether’s “trust us, bro” vibes, the value of fiat-backed stablecoins depends on centralized actors not screwing it up.

🤔 Stability ≠ safety. Even “stable” coins have broken their peg during macro shocks. If you’re counting on them to hold the line in a crisis, know what backs your bags, or brace for impact.

How Do Stablecoins Maintain Value?

At their heart, stablecoins work through a combination of pegging and collateralization. By anchoring 1:1 to a fiat currency (most commonly the U.S. dollar), stablecoins are designed to mimic the price stability of sovereign currency, while offering the advantages of digital assets.

There are three core ways stablecoins attempt to maintain their peg:

💰 Fiat-backed: 1 $USDC is backed by 1 actual U.S. dollar or dollar-equivalent held in reserves. These are regularly audited and visible to regulators and investors.

🧱Crypto-backed: Coins like $DAI use smart contracts to lock up crypto assets (like $ETH) at higher collateral ratios, making them more decentralized but less resistant to sharp drawdowns.

🧮 Algorithmic: Peg managed by smart contract rules and incentives, but often unstable in practice, particularly under extreme pressure (case study: TerraUSD).

A reliable peg isn’t just a technical curiosity. It’s the linchpin for trust. Without it, you’re at risk of holding a dollar on paper that trades like a penny stock on-chain.

Types of Stablecoins: Fiat vs Crypto-Backed

Not all stablecoins are created equal. The term suggests uniformity (tokens pegged to $1) but the way that peg is maintained varies widely, and it makes all the difference.

As we’ve learned above, some are backed by actual dollars, others rely on overcollateralized crypto, and a few still try to automate stability entirely through code.

The mechanism matters more than the marketing because when the market turns volatile, that $1 promise gets tested, and the consequence of failing that test can be disastrous.

Fiat-backed Stablecoins: Credible, Liquid, and Favored by Institutions

Institution-grade stablecoins like USDC and USDT are backed by reserves in traditional financial accounts.

These are the most liquid and widely accepted in trading pairs, DeFi protocols, and OTC desks.

What sets them apart is access to the real banking system, which is something decentralized alternatives can’t replicate, yet.

This direct fiat backing makes them both more trusted by institutions and more scrutinized by regulators.

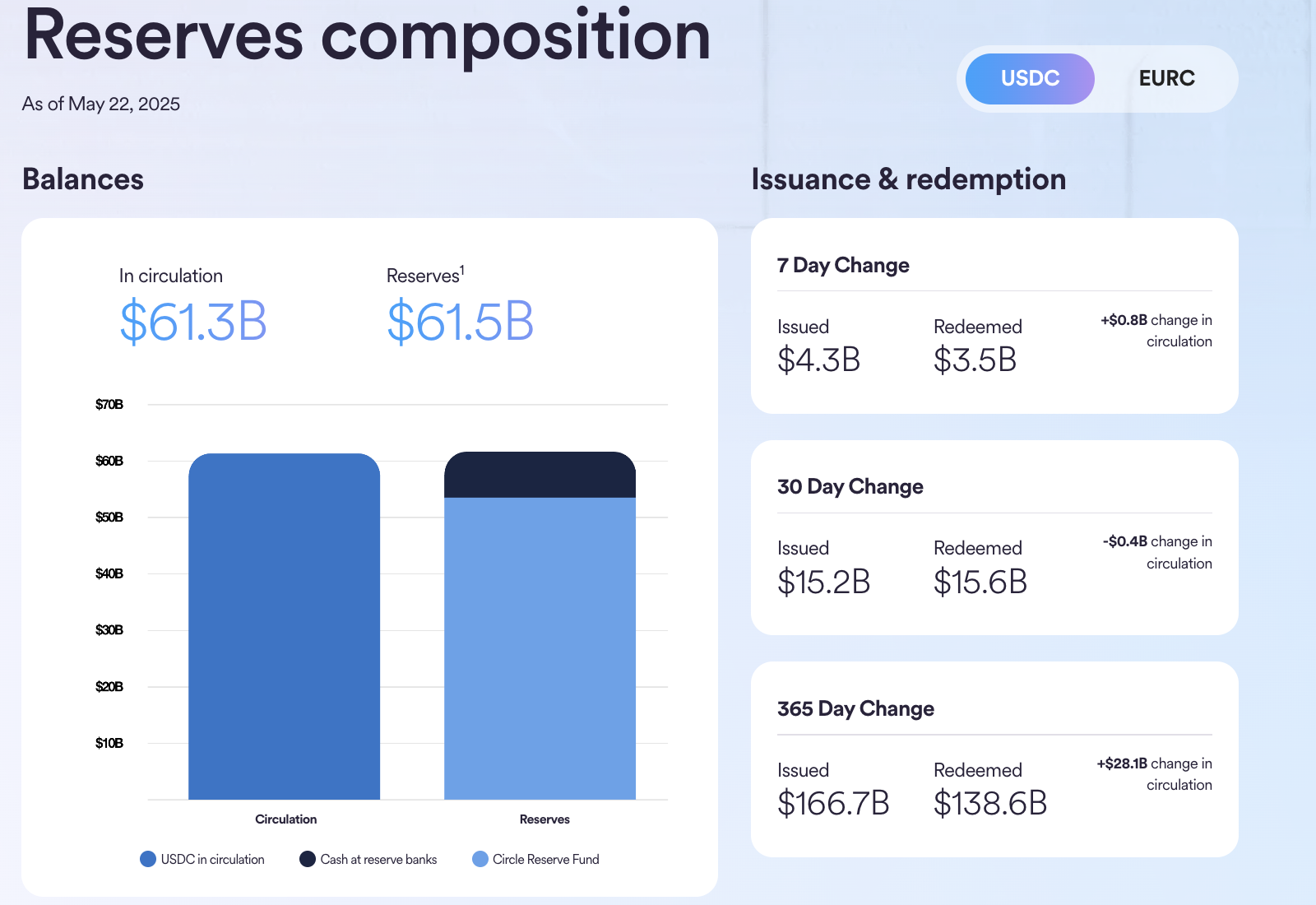

USD Coin( $USDC) issued by Circle, in partnership with Coinbase under the Centre Consortium, is fully reserved and transparent. Backed 1:1 with U.S. dollars and short-term U.S. Treasuries, USDC publishes monthly attestation reports verified by top accounting firms.

With its regulatory-first approach and partnerships with BlackRock, MoneyGram, Visa, and other blue-chip players, $USDC is the poster child for compliant digital dollars. It’s increasingly being used beyond crypto trading, in treasury operations, cross-border payments, and DeFi integrations.

Circle also posts real-time visuals of its reserve composition on this page.

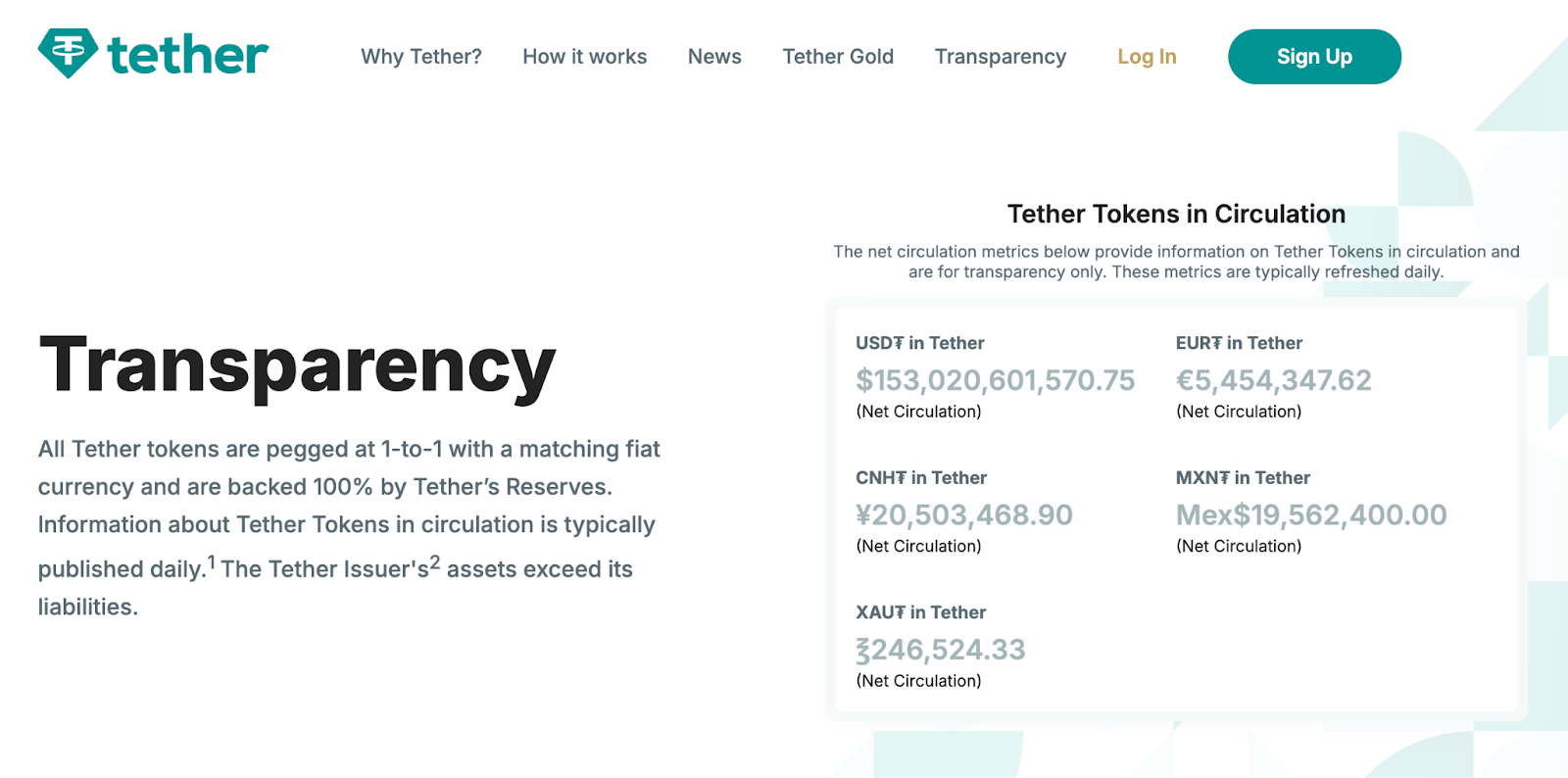

Tether’s $USDT is the largest stablecoin by market cap and trading volume. While reportedly fully reserved, its backing historically included a mix of commercial paper, cash, and other assets, raising questions about transparency.

Tether has since taken steps to reduce risk exposure and increase transparency through quarterly attestations.

Despite past scrutiny, $USDT remains the go-to liquidity proxy across centralized exchanges, particularly in Asia and emerging markets.

Crypto-backed Stablecoins: Decentralization Meets Volatility

MakerDAO’s $DAI is the most well-known example of a crypto-collateralized stablecoin. To mint $DAI, users lock up crypto assets like ETH in a smart contract worth more than the DAI issued, typically a 150%+ overcollateralization.

While more philosophically aligned with decentralization ideals, these models are less scalable and can lose peg parity under sharp market swings.

Algorithmic Stablecoins: Proceed With Caution

These stablecoins attempt to maintain their value through code-driven monetary policy: expanding or contracting supply dynamically.

The now-infamous collapse of TerraUSD ($UST) in mid-2022 wiped out billions, showing how these models can unravel without hard asset backing.

$UST was an algorithmic stablecoin designed to maintain its $1 peg using a burn-and-mint mechanism with its sister token, $LUNA. When $UST demand dropped, the system printed more $LUNA to absorb the sell pressure and restore the peg.

But as redemptions spiked and trust evaporated, the price of $LUNA collapsed, triggering a death spiral. Hyperinflation kicked in, the peg snapped, and over $40 billion in market value vanished in a matter of days. There were no real reserves: just code and confidence.

Once one broke, the other followed.

Institutional faith in algorithmic pegs is near zero, and regulatory support is minimal.

Types of Stablecoin Examples That Matter: For Traders and Investors

For the vast majority of use cases, stablecoins are typically used to momentarily hold dollar-pegged asset and move it between platforms, positions, or counterparties without exiting into the traditional banking system.

They serve as a kind of digital cash buffer: letting users lock in dollar value without sacrificing speed, custody, or on-chain composability. Whether you’re hedging during volatility, bridging to another chain, or waiting on the next entry point, stablecoins let you stay liquid, dollar-denominated, and crypto-native, all at once.

But, stablecoins aren’t just a convenient way to sit out volatility. For serious investors and active traders, they’re what keep the engine running. They smooth out trades, provide a stable unit of account, and make it possible to move between assets or across blockchains without off-ramping to fiat.

Stablecoins also unlock opportunities that would otherwise be gated behind banking hours or geography. They’re the base layer for DeFi protocols, OTC settlements, and automated treasury workflows.

They allow users to stay liquid, flexible, and globally operable, whether you’re parking funds before a move or routing large sums between wallets and exchanges.

And while we won’t dive deep into the yield mechanics here, know this: stablecoins aren’t always idle. In the right setup, they can generate yield (and take on the risk to do so.)

Whether that’s through liquidity provision, lending markets, or more advanced strategies, stablecoins often function as both a hedge and an opportunity.

More broadly, they represent something fiat still struggles with: portability. A stablecoin can be sent globally, settle in seconds, and plug into protocols that fiat never touches. That kind of access changes how people trade, but also how they earn, pay, and build.

How Stablecoin Companies Make Money

Let’s be clear, stablecoin issuers aren’t running nonprofits. They’re actually some of the most profitable companies, and not just in crypto.

Their model is simple, but the scale makes it lucrative. When someone converts dollars into a stablecoin like $USDC, that real-world cash doesn’t sit idle: it gets parked in extremely conservative low-risk assets like short-term treasuries and money market funds. The issuer keeps the yield.

Users get the dollar peg; the company keeps the interest.

Let’s break it down even further:

- When you buy 10,000 $USDC, Circle holds $10,000 in reserves (usually in short-term Treasuries or cash equivalents) to back it.

- You get a digital token ($USDC) to move around crypto markets. But Circle still holds the real $10,000.

- That $10,000 becomes part of the a pool of customer funds they can earn yield on. Since these reserves are often parked in 4–5% yielding government securities, your $10,000 is making Circle about $400 to $500 per year.

In bull markets, “float” can balloon into tens of billions. $50 billion float could generate $2–2.5 billion a year in passive revenue.

That’s a lot of passive income for Circle, Tether, and others just for holding customer deposits in low-risk instruments. Unlike banks, they’re not lending out your money: they’re profiting from the safest assets on earth.

And because most stablecoins aren’t FDIC-insured, issuers aren’t bound by the same capital requirements. It’s a leaner model with fewer obligations and a global reach.

For example, Circle, the issuer of USDC, reported a revenue of $1.68 billion in 2024, up from $1.45 billion in 2023.

Tether ($USDT), Tether, the largest stablecoin issuer, reported a staggering profit of $13 billion in 2024, more than double its $6.2 billion profit in 2023. At the end of 2024, Tether held over $113 billion in U.S. Treasuries, positioning it among the largest holders globally.

Tether even quietly out-earned BlackRock in the same year, pulling in $13 billion in net profit, more than double BlackRock’s $5.5 billion. What makes this figure astounding is that BlackRock is the world’s largest asset manager, managing over $10 trillion in assets for clients and collects fees.

Tether just holds the float. It parked over $113 billion, mostly in U.S. Treasuries, and kept the yield. No investors to pay. No complex product lines. Just a lean team and the most profitable digital dollar engine on earth.

So, that’s the “why” for that “what are stablecoins” question, if you truly want to follow the money.

The Pros and Cons of Stablecoins

Stablecoins have become crypto’s default unit of account, and for good reason. They offer fast settlement, minimal friction across platforms, and predictable value in a volatile market.

For traders, they’re the go-to rail for moving capital.

For investors, they serve as dollar-denominated exposure without exiting the ecosystem.

Platforms like Echo even route real-yield directly through stablecoin balances, making them productive assets, not just digital cash.

Since stablecoins like $USDC and $USDT effectively act as the base currency for crypto (most crypto trades route through stablecoin pairs), that means a huge chunk of crypto’s liquidity relies on just two private companies (Circle and Tether) both of which can freeze funds or blacklist wallets.

It’s highly uncommon they do, typically related to a government demand, but it’s still a flaw in the eyes of the hardcore decentralized crowd, who see it as part of a structural risk.

If $USDC or $USDT were compromised, depegged, or politically pressured, a huge portion of the crypto economy would seize up. In effect, it turns an open ecosystem into one chokepoint away from failure.

Final Thoughts: What Are Stablecoins and How Do They Maintain Value?

If Bitcoin’s a rollercoaster, stablecoins are the monorail, at least the custodied types of stablecoins.

Institution-grade stablecoins are evolving into integral tech for modern finance, and have quietly become one of the most consequential financial technologies of the last decade.

Stablecoins like $USDC, and to a more opaque extent $USDT, are reshaping how dollars move, settle, and store value at internet speed.

The implications here are enormous.

In underbanked regions, where dollar access is scarce, stablecoins can deliver dollar-like purchasing power to a blockchain wallet. For treasuries and trading desks, they offer dollar stability with efficient liquidity.

For the broader financial system, they offer a faster, cheaper settlement layer that could eventually challenge legacy payment rails, such as SWIFT. This isn’t just a crypto thing. It’s a financial infrastructure thing.

Stablecoins are digital assets built to do something most cryptocurrencies can’t: stay stable.

Pegged to a fiat currency, usually the U.S. dollar, they’re designed to hold value even when the rest of the market swings wildly.

They aim to consistently hold a fixed value, usually 1 US dollar, regardless of market turbulence.

That price stability makes them useful for everything from fast trading and cheap cross-border payments to staying in cash without actually leaving crypto.

Traders use them to hedge or move capital efficiently. DeFi protocols use them as base liquidity.

And increasingly, institutions use them to settle millions in volume without touching a bank.

They’ve quietly become one of the most important building blocks in digital finance. But behind the $1 peg, there’s a lot going on: and not every stablecoin is built the same way.

Some are backed by actual dollars. Others rely on smart contracts. A few run entirely on algorithms, and sometimes fall apart.

As regulation heats up and the financial world inches closer to tokenized dollars, understanding how stablecoins work isn’t optional. It’s foundational.

Let’s break down how they hold value, why investors care, and where they might fit into the next phase of global finance.

Why This Matters for You:

✅ You get a volatility-free tool in a market built on chaos. Stablecoins give you staying power (earning, lending, hedging) without having to YOLO your savings into whatever altcoin Twitter’s shilling today.

✅ You can trade like a sniper, not a bagholder. Stablecoins let you exit risk assets in seconds without leaving the crypto ecosystem, giving you firepower for the next play without touching your bank account.

✅ You unlock next-gen finance at your own pace. From staking in DeFi to sending cash across borders in less than a minute, stablecoins are the utility layer powering the real, usable side of crypto.

🤔 Trust isn’t programmable. Whether it’s Circle’s audits or Tether’s “trust us, bro” vibes, the value of fiat-backed stablecoins depends on centralized actors not screwing it up.

🤔 Stability ≠ safety. Even “stable” coins have broken their peg during macro shocks. If you’re counting on them to hold the line in a crisis, know what backs your bags, or brace for impact.

How Do Stablecoins Maintain Value?

At their heart, stablecoins work through a combination of pegging and collateralization. By anchoring 1:1 to a fiat currency (most commonly the U.S. dollar), stablecoins are designed to mimic the price stability of sovereign currency, while offering the advantages of digital assets.

There are three core ways stablecoins attempt to maintain their peg:

💰 Fiat-backed: 1 $USDC is backed by 1 actual U.S. dollar or dollar-equivalent held in reserves. These are regularly audited and visible to regulators and investors.

🧱Crypto-backed: Coins like $DAI use smart contracts to lock up crypto assets (like $ETH) at higher collateral ratios, making them more decentralized but less resistant to sharp drawdowns.

🧮 Algorithmic: Peg managed by smart contract rules and incentives, but often unstable in practice, particularly under extreme pressure (case study: TerraUSD).

A reliable peg isn’t just a technical curiosity. It’s the linchpin for trust. Without it, you’re at risk of holding a dollar on paper that trades like a penny stock on-chain.

Types of Stablecoins: Fiat vs Crypto-Backed

Not all stablecoins are created equal. The term suggests uniformity (tokens pegged to $1) but the way that peg is maintained varies widely, and it makes all the difference.

As we’ve learned above, some are backed by actual dollars, others rely on overcollateralized crypto, and a few still try to automate stability entirely through code.

The mechanism matters more than the marketing because when the market turns volatile, that $1 promise gets tested, and the consequence of failing that test can be disastrous.

Fiat-backed Stablecoins: Credible, Liquid, and Favored by Institutions

Institution-grade stablecoins like USDC and USDT are backed by reserves in traditional financial accounts.

These are the most liquid and widely accepted in trading pairs, DeFi protocols, and OTC desks.

What sets them apart is access to the real banking system, which is something decentralized alternatives can’t replicate, yet.

This direct fiat backing makes them both more trusted by institutions and more scrutinized by regulators.

USD Coin( $USDC) issued by Circle, in partnership with Coinbase under the Centre Consortium, is fully reserved and transparent. Backed 1:1 with U.S. dollars and short-term U.S. Treasuries, USDC publishes monthly attestation reports verified by top accounting firms.

With its regulatory-first approach and partnerships with BlackRock, MoneyGram, Visa, and other blue-chip players, $USDC is the poster child for compliant digital dollars. It’s increasingly being used beyond crypto trading, in treasury operations, cross-border payments, and DeFi integrations.

Circle also posts real-time visuals of its reserve composition on this page.

Tether’s $USDT is the largest stablecoin by market cap and trading volume. While reportedly fully reserved, its backing historically included a mix of commercial paper, cash, and other assets, raising questions about transparency.

Tether has since taken steps to reduce risk exposure and increase transparency through quarterly attestations.

Despite past scrutiny, $USDT remains the go-to liquidity proxy across centralized exchanges, particularly in Asia and emerging markets.

Crypto-backed Stablecoins: Decentralization Meets Volatility

MakerDAO’s $DAI is the most well-known example of a crypto-collateralized stablecoin. To mint $DAI, users lock up crypto assets like ETH in a smart contract worth more than the DAI issued, typically a 150%+ overcollateralization.

While more philosophically aligned with decentralization ideals, these models are less scalable and can lose peg parity under sharp market swings.

Algorithmic Stablecoins: Proceed With Caution

These stablecoins attempt to maintain their value through code-driven monetary policy: expanding or contracting supply dynamically.

The now-infamous collapse of TerraUSD ($UST) in mid-2022 wiped out billions, showing how these models can unravel without hard asset backing.

$UST was an algorithmic stablecoin designed to maintain its $1 peg using a burn-and-mint mechanism with its sister token, $LUNA. When $UST demand dropped, the system printed more $LUNA to absorb the sell pressure and restore the peg.

But as redemptions spiked and trust evaporated, the price of $LUNA collapsed, triggering a death spiral. Hyperinflation kicked in, the peg snapped, and over $40 billion in market value vanished in a matter of days. There were no real reserves: just code and confidence.

Once one broke, the other followed.

Institutional faith in algorithmic pegs is near zero, and regulatory support is minimal.

Types of Stablecoin Examples That Matter: For Traders and Investors

For the vast majority of use cases, stablecoins are typically used to momentarily hold dollar-pegged asset and move it between platforms, positions, or counterparties without exiting into the traditional banking system.

They serve as a kind of digital cash buffer: letting users lock in dollar value without sacrificing speed, custody, or on-chain composability. Whether you’re hedging during volatility, bridging to another chain, or waiting on the next entry point, stablecoins let you stay liquid, dollar-denominated, and crypto-native, all at once.

But, stablecoins aren’t just a convenient way to sit out volatility. For serious investors and active traders, they’re what keep the engine running. They smooth out trades, provide a stable unit of account, and make it possible to move between assets or across blockchains without off-ramping to fiat.

Stablecoins also unlock opportunities that would otherwise be gated behind banking hours or geography. They’re the base layer for DeFi protocols, OTC settlements, and automated treasury workflows.

They allow users to stay liquid, flexible, and globally operable, whether you’re parking funds before a move or routing large sums between wallets and exchanges.

And while we won’t dive deep into the yield mechanics here, know this: stablecoins aren’t always idle. In the right setup, they can generate yield (and take on the risk to do so.)

Whether that’s through liquidity provision, lending markets, or more advanced strategies, stablecoins often function as both a hedge and an opportunity.

More broadly, they represent something fiat still struggles with: portability. A stablecoin can be sent globally, settle in seconds, and plug into protocols that fiat never touches. That kind of access changes how people trade, but also how they earn, pay, and build.

How Stablecoin Companies Make Money

Let’s be clear, stablecoin issuers aren’t running nonprofits. They’re actually some of the most profitable companies, and not just in crypto.

Their model is simple, but the scale makes it lucrative. When someone converts dollars into a stablecoin like $USDC, that real-world cash doesn’t sit idle: it gets parked in extremely conservative low-risk assets like short-term treasuries and money market funds. The issuer keeps the yield.

Users get the dollar peg; the company keeps the interest.

Let’s break it down even further:

- When you buy 10,000 $USDC, Circle holds $10,000 in reserves (usually in short-term Treasuries or cash equivalents) to back it.

- You get a digital token ($USDC) to move around crypto markets. But Circle still holds the real $10,000.

- That $10,000 becomes part of the a pool of customer funds they can earn yield on. Since these reserves are often parked in 4–5% yielding government securities, your $10,000 is making Circle about $400 to $500 per year.

In bull markets, “float” can balloon into tens of billions. $50 billion float could generate $2–2.5 billion a year in passive revenue.

That’s a lot of passive income for Circle, Tether, and others just for holding customer deposits in low-risk instruments. Unlike banks, they’re not lending out your money: they’re profiting from the safest assets on earth.

And because most stablecoins aren’t FDIC-insured, issuers aren’t bound by the same capital requirements. It’s a leaner model with fewer obligations and a global reach.

For example, Circle, the issuer of USDC, reported a revenue of $1.68 billion in 2024, up from $1.45 billion in 2023.

Tether ($USDT), Tether, the largest stablecoin issuer, reported a staggering profit of $13 billion in 2024, more than double its $6.2 billion profit in 2023. At the end of 2024, Tether held over $113 billion in U.S. Treasuries, positioning it among the largest holders globally.

Tether even quietly out-earned BlackRock in the same year, pulling in $13 billion in net profit, more than double BlackRock’s $5.5 billion. What makes this figure astounding is that BlackRock is the world’s largest asset manager, managing over $10 trillion in assets for clients and collects fees.

Tether just holds the float. It parked over $113 billion, mostly in U.S. Treasuries, and kept the yield. No investors to pay. No complex product lines. Just a lean team and the most profitable digital dollar engine on earth.

So, that’s the “why” for that “what are stablecoins” question, if you truly want to follow the money.

The Pros and Cons of Stablecoins

Stablecoins have become crypto’s default unit of account, and for good reason. They offer fast settlement, minimal friction across platforms, and predictable value in a volatile market.

For traders, they’re the go-to rail for moving capital.

For investors, they serve as dollar-denominated exposure without exiting the ecosystem.

Platforms like Echo even route real-yield directly through stablecoin balances, making them productive assets, not just digital cash.

Since stablecoins like $USDC and $USDT effectively act as the base currency for crypto (most crypto trades route through stablecoin pairs), that means a huge chunk of crypto’s liquidity relies on just two private companies (Circle and Tether) both of which can freeze funds or blacklist wallets.

It’s highly uncommon they do, typically related to a government demand, but it’s still a flaw in the eyes of the hardcore decentralized crowd, who see it as part of a structural risk.

If $USDC or $USDT were compromised, depegged, or politically pressured, a huge portion of the crypto economy would seize up. In effect, it turns an open ecosystem into one chokepoint away from failure.

Final Thoughts: What Are Stablecoins and How Do They Maintain Value?

If Bitcoin’s a rollercoaster, stablecoins are the monorail, at least the custodied types of stablecoins.

Institution-grade stablecoins are evolving into integral tech for modern finance, and have quietly become one of the most consequential financial technologies of the last decade.

Stablecoins like $USDC, and to a more opaque extent $USDT, are reshaping how dollars move, settle, and store value at internet speed.

The implications here are enormous.

In underbanked regions, where dollar access is scarce, stablecoins can deliver dollar-like purchasing power to a blockchain wallet. For treasuries and trading desks, they offer dollar stability with efficient liquidity.

For the broader financial system, they offer a faster, cheaper settlement layer that could eventually challenge legacy payment rails, such as SWIFT. This isn’t just a crypto thing. It’s a financial infrastructure thing.