What Is Ripple Crypto ($XRP)? Everything You Need to Know

So you’re wondering what Ripple is, besides the crypto that banks don’t hate. Fair question.

Ripple (the company) and $XRP (the token) have spent the last decade attempting to speed up global payments radically. But somewhere along the way, Ripple got called a crypto disruptor, a centralized villain, a banker’s dream, and even a security by the SEC.

That’s a lot of heat for a company building a faster payments rail.

Here’s the deal: Ripple is an enterprise blockchain firm. $XRP is a digital token that lubricates its money-moving machine, especially across borders. If Bitcoin is a decentralized digital gold, Ripple is more like a sleek API for transnational finance, offering frictionless currency exchange and instant settlement.

Now let’s unpack what this actually means for you, whether you’re a beginner, DeFi native, or a fintech ops manager wondering if $XRP replaces SWIFT.

Why this matters for you:

✅ It could lead to faster cross-border payments through institutions.

✅ Institutions can unlock dormant cash instead of parking funds in multiple countries.

✅ $XRP brings real-world FX utility to crypto.

🤔 Ripple still controls a huge stash of $XRP, which raises centralization questions.

🤔 SEC-regulatory limbo could limit adoption, partnerships, and how $XRP trades in the U.S.

So, What Is Ripple? About the Company

Ripple is a blockchain-adjacent fintech company founded in 2012 that builds payment infrastructure. Its signature protocol is RippleNet, a ledger-based solution for messaging and clearing transactions across borders.

Unlike traditional rails (think SWIFT), RippleNet settles in seconds, not days.

$XRP, meanwhile, is the digital asset that enables this magic. It’s used inside RippleNet’s On-Demand Liquidity (ODL) functionality to bridge currencies.

Think of $XRP as a real-time bridge asset. It lets institutions send USD and instantly convert it to MXN (or any other fiat) by using $XRP as the middle link.

Ripple’s story actually begins in 2004, when Canadian developer Ryan Fugger launched a project called RipplePay, a decentralized system for individuals to issue credit to one another. Fugger is often left out of the $XRP-focused narrative because his role was tied to an earlier, unrelated version of the project.

This version of RipplePay wasn’t blockchain-based, but it laid the philosophical groundwork for what would come next.

In 2011, a new technical team, David Schwartz, Jed McCaleb, and Arthur Britto, built the $XRP Ledger, designed from the ground up to move value quickly and securely. This a trio of cryptography-heavy hitters approached Fugger, who passed the RipplePay torch.

In 2012, they brought on entrepreneur Chris Larsen to help formalize the company and bring it to market.

McCaleb eventually left to found Stellar, but the core tech still runs on the same principles they designed over a decade ago.

Today, Ripple is led by Brad Garlinghouse (CEO), a Silicon Valley veteran who joined in 2015 and took the helm a year later. David Schwartz (CTO) remains the technical brains behind the operation, and Chris Larsen serves as Executive Chairman, steering Ripple’s broader vision.

The leadership bench also includes Monica Long (President) and Stuart Alderoty (Chief Legal Officer), key players in Ripple’s recent legal wins and expansion push.

Ripple vs $XRP: What’s the Real Difference?

Ripple is the company. $XRP is the token that it helped develop and now supports.

This confusion was partly by design. Ripple initially distributed tons of $XRP to itself and its founders, then claimed the token is independent because it “runs on an open-source ledger.”

The reality is more nuanced.

In its early years, Ripple issued 100 billion $XRP, kept a huge portion for itself and its founders, and began positioning the token as an “independent digital asset.”

The claim? $XRP runs on a decentralized, open-source ledger, separate from any one company.

Technically true. But also conveniently framed.

As of 2025, around 59 billion $XRP are in active circulation, while approximately 41 billion remain in Ripple’s escrow. The monthly net increase in circulating supply tends to range between 100 to 300 million $XRP, depending on how much Ripple uses or returns to escrow. These flows are visible on-chain and governed by smart contract logic built into the $XRP Ledger.

Ripple is also deeply involved in guiding $XRP Ledger upgrades, even if it doesn’t control validator nodes like Bitcoin miners. This dual role, cheerleader and stakeholder, has sparked years of debate:

Warning

Critics say the company can’t have it both ways. You can’t hold a war chest of $XRP, sell it to fund your business, and then claim you’re not responsible for how it’s used or governed.

Defenders argue Ripple’s involvement is what gives $XRP practical utility. Without a company like Ripple pushing adoption, the token might’ve faded into crypto obscurity alongside dozens of other altcoins.

The SEC lawsuit that started in 2020 leaned heavily on this tension. Regulators claimed $XRP was a security because Ripple sold it while controlling its supply and marketing narrative. In 2023 and 2025 rulings, courts disagreed—at least for retail sales—but the case underscored the blurred lines between “decentralized asset” and “corporate treasury.”

The Ripple company still holds a massive amount of $XRP (over 40 billion tokens in escrow) and helps guide $XRP Ledger upgrades, even if it doesn’t control nodes like Bitcoin miners do.

How Does $XRP Work Under the Hood?

If Bitcoin uses mining and Proof-of-Work to validate transactions, $XRP is more like a digital voting ring.

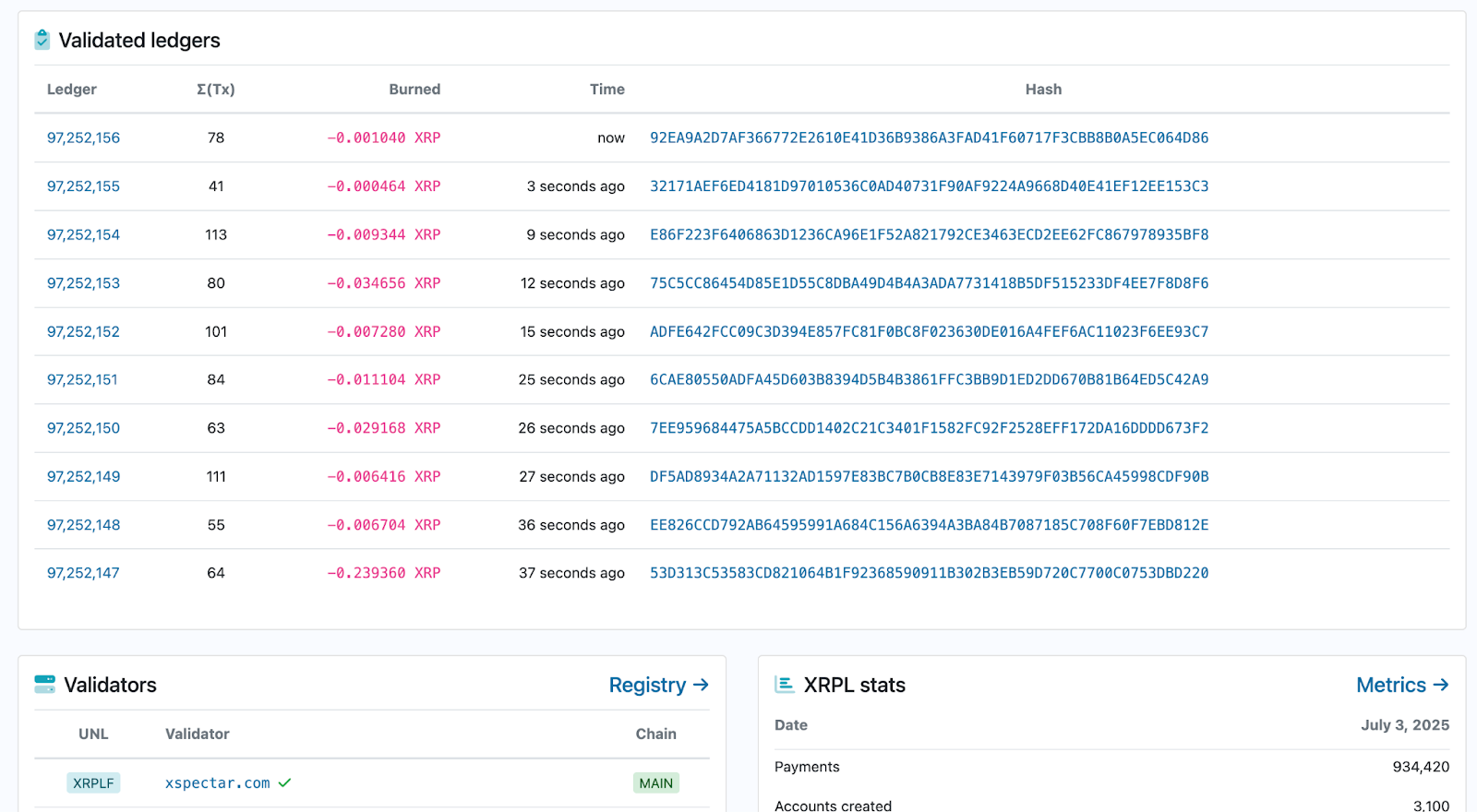

$XRP Ledger replaces mining with a unique consensus protocol. Here, independent validators (including universities, exchanges, and, yes, Ripple itself) agree on the state of transactions every few seconds. There are no rewards like bitcoin mining blocks, validators run servers to maintain the network efficiently and cheaply.

No mining means $XRP is fast. A typical transaction is confirmed in 3 to 5 seconds. Fees are mere fractions of a cent.

RippleNet and On-Demand Liquidity: What’s the Hook?

The $XRP Ledger is foundational, but RippleNet is where it gets specific. RippleNet is a permissioned suite for banks and payment service providers, like an upgraded SWIFT backed by blockchain settlement.

In some corridors, Ripple enables On-Demand Liquidity (ODL), where institutions (like MoneyGram used to) use $XRP to bridge currencies instantly. Instead of pre-funding accounts in each country, partners use $XRP to sidestep delays and FX friction.

Tokenomics: The $XRP Ledger’s Supply Story

$XRP was launched in June 2012 with a fixed supply of 100 billion tokens, all pre-mined, no mining, no inflation, and designed to fuel global payments more efficiently.

Ripple received 80 billion $XRP to fund its ecosystem; the remaining 20 billion went to founders and early contributors. In late 2017, Ripple placed 55 billion $XRP into escrow, creating a monthly unlock schedule to ensure transparency and control.

- Total supply: 100 billion $XRP

Escrowed (locked): ~40 to 41 billion $XRP (as of mid‑2025)

Circulating supply: ~59 billion $XRP (~59% of max)

Monthly unlock: 1 billion $XRP, with unused amounts typically re-escrowed

The escrow mechanism adds predictability: each month, 1 billion $XRP becomes available; if unused, it returns to escrow.

XRP also features a micro-burn on each transaction, introducing minimal deflation into an otherwise static supply. However, these burns are tiny compared to the escrow flow, so the overall supply remains essentially capped.

The escrow schedule offers transparent tokenomics, which investors can track via tools like XRPSCAN and Messari.

Real-World Use Cases for $XRP

Sending money across borders is a $600+ billion industry mired in delays and fees. $XRP shines for global remittances where small local currencies (Philippine Peso, Mexican Peso) are involved.

Some corporations explore using $XRP to shuttle idle capital between regions or subsidiaries. It’s early, but Ripple has offered $XRP-based liquidity to firms needing real-time working capital flows.

In volatile or isolated fiat markets, $XRP offers a pseudo-stable, extremely liquid on-ramp. There’s also noise around $XRP for streaming microtransactions (think pay-per-second video), but the developer stack still lags Ethereum.

What makes Ripple different from other blockchain projects focused on banking?

Most blockchain projects tackling finance either compete with banks or aim to bypass them entirely. Ripple’s approach is to work directly with traditional financial institutions to upgrade the back-end of global money movement systems, not replace them.

If Ethereum is trying to reinvent finance from scratch, Ripple is updating the cables behind the wall. It’s infrastructure-level plumbing that lets banks and fintechs move money more efficiently, using $XRP as a neutral bridge asset.

Key differences include Ripple’s focus on compliance-friendly, scalable systems optimized for regulated environments. Unlike public blockchains trying to do everything at once, Ripple zeroes in on solving foreign exchange friction in cross-border settlements. RippleNet and the $XRP Ledger are purpose-built for enterprises in payment rails, not for building dApps or DeFi protocols.

Can $XRP be used for stablecoin settlement on private blockchains?

Yes, $XRP can be used to settle stablecoin transactions even on private or permissioned versions of the $XRP Ledger. Ripple has explored pilot programs and sidechain development that allow banks, fintechs, or governments to issue their own stablecoins or digital currencies while using $XRP for interoperability and liquidity.

Imagine a network of walled gardens (private ledgers) needing a trustworthy courier ($XRP) to move value between them. $XRP acts as that liquid clearing asset, enabling rapid stablecoin exchanges across otherwise siloed systems.

For example, a private ledger for a bank-issued CBDC could still connect back to the public $XRP Ledger or to other institutions by using $XRP as a bridge asset. Ripple’s support for this comes from the platform’s low cost, sub-second transaction times, and scalable architecture, which are crucial for stable settlement performance.

This flexibility makes $XRP a potential settlement layer not only for crypto-native tokens but for tokenized fiat on institutional rails.

How is Ripple working with central banks on CBDC technology?

Ripple is working directly with several central banks to pilot custom blockchain infrastructure for Central Bank Digital Currencies (CBDCs). These projects often use versions of the $XRP Ledger tailored for privacy, control, and issuance needs specific to public monetary systems.

Think of it as Ripple offering a sandbox where central banks can test issuing and managing digital currencies without starting from zero. The same tech stack that powers the public $XRP Ledger can be mirrored in private environments, with guardrails for compliance, identity, and governance.

Ripple’s CBDC platform already has pilot programs underway with countries like Palau and Bhutan. These initiatives focus on improving financial inclusion, streamlining citizen-to-government payments, and future-proofing legacy banking rails. While $XRP itself isn’t the CBDC, the underlying tech and optional use of $XRP for cross-border clearing add real utility.

Does Ripple’s legal clarity in the U.S. Change how $XRP is integrated in fintech platforms?

Yes, Ripple’s partial legal clarity in the U.S. has removed a major uncertainty that kept fintech platforms hesitant to use $XRP. A federal court ruling in 2023 stated that $XRP is not a security in secondary market sales (like on exchanges), which opens the door for broader integration.

It’s like finally knowing whether a product you want to carry is legal in your store. With that clarity, fintechs can confidently build on or integrate with $XRP without fearing regulatory surprises, at least in the U.S.

This paves the way for wallets, payment apps, and enterprise APIs to leverage $XRP for liquidity or settlement functions. While the legal landscape is still evolving, this ruling has already led to several U.S. exchanges relisting $XRP and hinted at more partnerships in the fintech space.

Ripple vs Bitcoin

Bitcoin aims to decentralize money and remove trust from the system. Ripple is trust-enabled: banks trust Ripple’s tools to make their internal systems smarter.

Bitcoin uses Proof-of-Work, a slow, secure, energy-heavy protocol. $XRP uses consensus among validators, fast, efficient, low energy, but arguably less trustless.

Bitcoin has 21 million coins, slowly mined. $XRP started with 100 billion pre-mined. Ripple still owns over 40% of that, locked in escrow, and released monthly to fund operations and partnerships.

Bitcoin is decentralized via open-source development and global miner distribution. $XRP Ledger is more dependent on Ripple’s influence, though it boasts third-party validators.

Both are useful, but for different goals. Bitcoin is freedom tech. Ripple is enterprise fintech.

What Are the Risks and Limitations of $XRP and Ripple?

$XRP offers speed and efficiency, but not without trade-offs, including centralization concerns, regulatory baggage, and long-term reliance on institutional adoption.

Centralization risk

Ripple isn’t fully decentralized, and the majority of $XRP is still controlled by Ripple or related parties. While letting banks settle faster, critics argue $XRP is more like a fintech token than a pure crypto asset.

Regulatory risk

The U.S. SEC (Securities and Exchange Commission) sued Ripple Labs in 2020 for allegedly selling $XRP as an unregistered security. Ripple contested it, arguing $XRP is a utility token, not equity. A 2023 ruling partially sided with Ripple, saying secondary sales don’t qualify as securities, but issues remain unresolved.

The long-running legal battle between Ripple and the U.S. SEC is effectively over. In June 2025, both Ripple and the SEC dropped their appeals, paving the way for the case to close formally. Ripple agreed to a $125 million penalty and continues to face restrictions on certain institutional $XRP sales.

Institutional buy-in

$XRP rides or dies on institutional uptake. If banks abandon RippleNet for other blockchain options or regulatory uncertainty scares them off, $XRP liquidity could suffer.

$XRP escrow and market dilution

Ripple releases up to 1 billion $XRP per month from escrow. While it doesn’t dump this all at once, holders worry constant supply overhang could suppress market prices and deter long-term traction.

Final Thoughts: What Is Ripple and What Does It Mean for You?

Ripple isn’t sexy. $XRP isn’t a meme. But that might be its edge. Ripple’s trying to replace the rusted bolts holding global payments together quietly. It’s an infrastructure play.

For crypto natives, that’s both cool and controversial. It trades ideological decentralization for serviceable utility. You can stake ETH and philosophize freedom, or use $XRP and move funds in 3 seconds flat.

Is it perfect? No. Is it doing something useful? Yes. Ripple didn’t ask permission from the crypto community, only from Basel and the Bank of America.

Comparing Ripple to decentralized peer-to-peer currencies like Bitcoin is apples to oranges; it’s a more apt comparison to weigh Ripple to Stellar Lumens ($XLM), another cross-border asset.

Or dive into the $XRP Ledger itself, run a validator, and test ODL on a devnet.

So you’re wondering what Ripple is, besides the crypto that banks don’t hate. Fair question.

Ripple (the company) and $XRP (the token) have spent the last decade attempting to speed up global payments radically. But somewhere along the way, Ripple got called a crypto disruptor, a centralized villain, a banker’s dream, and even a security by the SEC.

That’s a lot of heat for a company building a faster payments rail.

Here’s the deal: Ripple is an enterprise blockchain firm. $XRP is a digital token that lubricates its money-moving machine, especially across borders. If Bitcoin is a decentralized digital gold, Ripple is more like a sleek API for transnational finance, offering frictionless currency exchange and instant settlement.

Now let’s unpack what this actually means for you, whether you’re a beginner, DeFi native, or a fintech ops manager wondering if $XRP replaces SWIFT.

Why this matters for you:

✅ It could lead to faster cross-border payments through institutions.

✅ Institutions can unlock dormant cash instead of parking funds in multiple countries.

✅ $XRP brings real-world FX utility to crypto.

🤔 Ripple still controls a huge stash of $XRP, which raises centralization questions.

🤔 SEC-regulatory limbo could limit adoption, partnerships, and how $XRP trades in the U.S.

So, What Is Ripple? About the Company

Ripple is a blockchain-adjacent fintech company founded in 2012 that builds payment infrastructure. Its signature protocol is RippleNet, a ledger-based solution for messaging and clearing transactions across borders.

Unlike traditional rails (think SWIFT), RippleNet settles in seconds, not days.

$XRP, meanwhile, is the digital asset that enables this magic. It’s used inside RippleNet’s On-Demand Liquidity (ODL) functionality to bridge currencies.

Think of $XRP as a real-time bridge asset. It lets institutions send USD and instantly convert it to MXN (or any other fiat) by using $XRP as the middle link.

Ripple’s story actually begins in 2004, when Canadian developer Ryan Fugger launched a project called RipplePay, a decentralized system for individuals to issue credit to one another. Fugger is often left out of the $XRP-focused narrative because his role was tied to an earlier, unrelated version of the project.

This version of RipplePay wasn’t blockchain-based, but it laid the philosophical groundwork for what would come next.

In 2011, a new technical team, David Schwartz, Jed McCaleb, and Arthur Britto, built the $XRP Ledger, designed from the ground up to move value quickly and securely. This a trio of cryptography-heavy hitters approached Fugger, who passed the RipplePay torch.

In 2012, they brought on entrepreneur Chris Larsen to help formalize the company and bring it to market.

McCaleb eventually left to found Stellar, but the core tech still runs on the same principles they designed over a decade ago.

Today, Ripple is led by Brad Garlinghouse (CEO), a Silicon Valley veteran who joined in 2015 and took the helm a year later. David Schwartz (CTO) remains the technical brains behind the operation, and Chris Larsen serves as Executive Chairman, steering Ripple’s broader vision.

The leadership bench also includes Monica Long (President) and Stuart Alderoty (Chief Legal Officer), key players in Ripple’s recent legal wins and expansion push.

Ripple vs $XRP: What’s the Real Difference?

Ripple is the company. $XRP is the token that it helped develop and now supports.

This confusion was partly by design. Ripple initially distributed tons of $XRP to itself and its founders, then claimed the token is independent because it “runs on an open-source ledger.”

The reality is more nuanced.

In its early years, Ripple issued 100 billion $XRP, kept a huge portion for itself and its founders, and began positioning the token as an “independent digital asset.”

The claim? $XRP runs on a decentralized, open-source ledger, separate from any one company.

Technically true. But also conveniently framed.

As of 2025, around 59 billion $XRP are in active circulation, while approximately 41 billion remain in Ripple’s escrow. The monthly net increase in circulating supply tends to range between 100 to 300 million $XRP, depending on how much Ripple uses or returns to escrow. These flows are visible on-chain and governed by smart contract logic built into the $XRP Ledger.

Ripple is also deeply involved in guiding $XRP Ledger upgrades, even if it doesn’t control validator nodes like Bitcoin miners. This dual role, cheerleader and stakeholder, has sparked years of debate:

Warning

Critics say the company can’t have it both ways. You can’t hold a war chest of $XRP, sell it to fund your business, and then claim you’re not responsible for how it’s used or governed.

Defenders argue Ripple’s involvement is what gives $XRP practical utility. Without a company like Ripple pushing adoption, the token might’ve faded into crypto obscurity alongside dozens of other altcoins.

The SEC lawsuit that started in 2020 leaned heavily on this tension. Regulators claimed $XRP was a security because Ripple sold it while controlling its supply and marketing narrative. In 2023 and 2025 rulings, courts disagreed—at least for retail sales—but the case underscored the blurred lines between “decentralized asset” and “corporate treasury.”

The Ripple company still holds a massive amount of $XRP (over 40 billion tokens in escrow) and helps guide $XRP Ledger upgrades, even if it doesn’t control nodes like Bitcoin miners do.

How Does $XRP Work Under the Hood?

If Bitcoin uses mining and Proof-of-Work to validate transactions, $XRP is more like a digital voting ring.

$XRP Ledger replaces mining with a unique consensus protocol. Here, independent validators (including universities, exchanges, and, yes, Ripple itself) agree on the state of transactions every few seconds. There are no rewards like bitcoin mining blocks, validators run servers to maintain the network efficiently and cheaply.

No mining means $XRP is fast. A typical transaction is confirmed in 3 to 5 seconds. Fees are mere fractions of a cent.

RippleNet and On-Demand Liquidity: What’s the Hook?

The $XRP Ledger is foundational, but RippleNet is where it gets specific. RippleNet is a permissioned suite for banks and payment service providers, like an upgraded SWIFT backed by blockchain settlement.

In some corridors, Ripple enables On-Demand Liquidity (ODL), where institutions (like MoneyGram used to) use $XRP to bridge currencies instantly. Instead of pre-funding accounts in each country, partners use $XRP to sidestep delays and FX friction.

Tokenomics: The $XRP Ledger’s Supply Story

$XRP was launched in June 2012 with a fixed supply of 100 billion tokens, all pre-mined, no mining, no inflation, and designed to fuel global payments more efficiently.

Ripple received 80 billion $XRP to fund its ecosystem; the remaining 20 billion went to founders and early contributors. In late 2017, Ripple placed 55 billion $XRP into escrow, creating a monthly unlock schedule to ensure transparency and control.

- Total supply: 100 billion $XRP

Escrowed (locked): ~40 to 41 billion $XRP (as of mid‑2025)

Circulating supply: ~59 billion $XRP (~59% of max)

Monthly unlock: 1 billion $XRP, with unused amounts typically re-escrowed

The escrow mechanism adds predictability: each month, 1 billion $XRP becomes available; if unused, it returns to escrow.

XRP also features a micro-burn on each transaction, introducing minimal deflation into an otherwise static supply. However, these burns are tiny compared to the escrow flow, so the overall supply remains essentially capped.

The escrow schedule offers transparent tokenomics, which investors can track via tools like XRPSCAN and Messari.

Real-World Use Cases for $XRP

Sending money across borders is a $600+ billion industry mired in delays and fees. $XRP shines for global remittances where small local currencies (Philippine Peso, Mexican Peso) are involved.

Some corporations explore using $XRP to shuttle idle capital between regions or subsidiaries. It’s early, but Ripple has offered $XRP-based liquidity to firms needing real-time working capital flows.

In volatile or isolated fiat markets, $XRP offers a pseudo-stable, extremely liquid on-ramp. There’s also noise around $XRP for streaming microtransactions (think pay-per-second video), but the developer stack still lags Ethereum.

What makes Ripple different from other blockchain projects focused on banking?

Most blockchain projects tackling finance either compete with banks or aim to bypass them entirely. Ripple’s approach is to work directly with traditional financial institutions to upgrade the back-end of global money movement systems, not replace them.

If Ethereum is trying to reinvent finance from scratch, Ripple is updating the cables behind the wall. It’s infrastructure-level plumbing that lets banks and fintechs move money more efficiently, using $XRP as a neutral bridge asset.

Key differences include Ripple’s focus on compliance-friendly, scalable systems optimized for regulated environments. Unlike public blockchains trying to do everything at once, Ripple zeroes in on solving foreign exchange friction in cross-border settlements. RippleNet and the $XRP Ledger are purpose-built for enterprises in payment rails, not for building dApps or DeFi protocols.

Can $XRP be used for stablecoin settlement on private blockchains?

Yes, $XRP can be used to settle stablecoin transactions even on private or permissioned versions of the $XRP Ledger. Ripple has explored pilot programs and sidechain development that allow banks, fintechs, or governments to issue their own stablecoins or digital currencies while using $XRP for interoperability and liquidity.

Imagine a network of walled gardens (private ledgers) needing a trustworthy courier ($XRP) to move value between them. $XRP acts as that liquid clearing asset, enabling rapid stablecoin exchanges across otherwise siloed systems.

For example, a private ledger for a bank-issued CBDC could still connect back to the public $XRP Ledger or to other institutions by using $XRP as a bridge asset. Ripple’s support for this comes from the platform’s low cost, sub-second transaction times, and scalable architecture, which are crucial for stable settlement performance.

This flexibility makes $XRP a potential settlement layer not only for crypto-native tokens but for tokenized fiat on institutional rails.

How is Ripple working with central banks on CBDC technology?

Ripple is working directly with several central banks to pilot custom blockchain infrastructure for Central Bank Digital Currencies (CBDCs). These projects often use versions of the $XRP Ledger tailored for privacy, control, and issuance needs specific to public monetary systems.

Think of it as Ripple offering a sandbox where central banks can test issuing and managing digital currencies without starting from zero. The same tech stack that powers the public $XRP Ledger can be mirrored in private environments, with guardrails for compliance, identity, and governance.

Ripple’s CBDC platform already has pilot programs underway with countries like Palau and Bhutan. These initiatives focus on improving financial inclusion, streamlining citizen-to-government payments, and future-proofing legacy banking rails. While $XRP itself isn’t the CBDC, the underlying tech and optional use of $XRP for cross-border clearing add real utility.

Does Ripple’s legal clarity in the U.S. Change how $XRP is integrated in fintech platforms?

Yes, Ripple’s partial legal clarity in the U.S. has removed a major uncertainty that kept fintech platforms hesitant to use $XRP. A federal court ruling in 2023 stated that $XRP is not a security in secondary market sales (like on exchanges), which opens the door for broader integration.

It’s like finally knowing whether a product you want to carry is legal in your store. With that clarity, fintechs can confidently build on or integrate with $XRP without fearing regulatory surprises, at least in the U.S.

This paves the way for wallets, payment apps, and enterprise APIs to leverage $XRP for liquidity or settlement functions. While the legal landscape is still evolving, this ruling has already led to several U.S. exchanges relisting $XRP and hinted at more partnerships in the fintech space.

Ripple vs Bitcoin

Bitcoin aims to decentralize money and remove trust from the system. Ripple is trust-enabled: banks trust Ripple’s tools to make their internal systems smarter.

Bitcoin uses Proof-of-Work, a slow, secure, energy-heavy protocol. $XRP uses consensus among validators, fast, efficient, low energy, but arguably less trustless.

Bitcoin has 21 million coins, slowly mined. $XRP started with 100 billion pre-mined. Ripple still owns over 40% of that, locked in escrow, and released monthly to fund operations and partnerships.

Bitcoin is decentralized via open-source development and global miner distribution. $XRP Ledger is more dependent on Ripple’s influence, though it boasts third-party validators.

Both are useful, but for different goals. Bitcoin is freedom tech. Ripple is enterprise fintech.

What Are the Risks and Limitations of $XRP and Ripple?

$XRP offers speed and efficiency, but not without trade-offs, including centralization concerns, regulatory baggage, and long-term reliance on institutional adoption.

Centralization risk

Ripple isn’t fully decentralized, and the majority of $XRP is still controlled by Ripple or related parties. While letting banks settle faster, critics argue $XRP is more like a fintech token than a pure crypto asset.

Regulatory risk

The U.S. SEC (Securities and Exchange Commission) sued Ripple Labs in 2020 for allegedly selling $XRP as an unregistered security. Ripple contested it, arguing $XRP is a utility token, not equity. A 2023 ruling partially sided with Ripple, saying secondary sales don’t qualify as securities, but issues remain unresolved.

The long-running legal battle between Ripple and the U.S. SEC is effectively over. In June 2025, both Ripple and the SEC dropped their appeals, paving the way for the case to close formally. Ripple agreed to a $125 million penalty and continues to face restrictions on certain institutional $XRP sales.

Institutional buy-in

$XRP rides or dies on institutional uptake. If banks abandon RippleNet for other blockchain options or regulatory uncertainty scares them off, $XRP liquidity could suffer.

$XRP escrow and market dilution

Ripple releases up to 1 billion $XRP per month from escrow. While it doesn’t dump this all at once, holders worry constant supply overhang could suppress market prices and deter long-term traction.

Final Thoughts: What Is Ripple and What Does It Mean for You?

Ripple isn’t sexy. $XRP isn’t a meme. But that might be its edge. Ripple’s trying to replace the rusted bolts holding global payments together quietly. It’s an infrastructure play.

For crypto natives, that’s both cool and controversial. It trades ideological decentralization for serviceable utility. You can stake ETH and philosophize freedom, or use $XRP and move funds in 3 seconds flat.

Is it perfect? No. Is it doing something useful? Yes. Ripple didn’t ask permission from the crypto community, only from Basel and the Bank of America.

Comparing Ripple to decentralized peer-to-peer currencies like Bitcoin is apples to oranges; it’s a more apt comparison to weigh Ripple to Stellar Lumens ($XLM), another cross-border asset.

Or dive into the $XRP Ledger itself, run a validator, and test ODL on a devnet.